Render vs. Akash: A Deeper Look Into Friendly Fire

To a crypto native, it should come as no surprise that the Render and Akash communities tend to express less than favorable feelings towards one another.

Sector animosity is commonplace in crypto, with tribes waging war in the comments sections, each side believing their protocol to be the savior who will single-handedly overthrow the centralized overlords in their sector.

As a Render-maxi, I wanted to know whether my own biases were blinding me and if Akash could turn out to be the better medium-term bet for decentralized GPU networks.

From my initial research, there didn’t seem to be any compelling text or video content detailing the similarities and differences between these two protocols or how they stacked up against centralized offerings. So, I figured there could possibly be a niche demand for a deeper dive.

The truth is, neither Akash or Render are close to capturing enough market share to elicit any serious concern from centralized competitors. Furthermore, there are fundamental differences between both protocols which suggest the term “competitor” may not be the correct way to describe their relationship to one another.

Instead of drinking the protocol-maxi kool aid (short-term tempting, long-term dangerous), let’s take a sober look at each of their positioning within the market and explore some data around their fundamental growth metrics.

Chapter Guide:

Compute Overview

Render vs. Akash

Positioning

Value Propositions

Growth Metrics

Concluding Thoughts

The State of Compute

In order to understand why decentralized compute networks matter, it’s helpful to have a basic understanding of the underlying tech. For the sake of readability, I’ll just cover CPUs and GPUs. There are other “PUs” which are very task specific like TPUs, but they’re not super relevant to crypto (yet).

The CPU is like the brain of the computer. It performs the essential computational tasks required for running software programs and managing system resources in a computer system. CPUs can handle a large variety of tasks and are really good at executing complex sequential computations that require extensive branching and logic.

Modern CPUs are made up of multiple “cores” (mini-processors). Each core can run its own task, allowing CPUs to perform sequential tasks in parallel. However, due to power consumption, heat dissipation and cost, the amount of cores you can reasonably put in a CPU is limited. Currently, high end consumer CPUs max out at around 64 cores.

GPUs on the other hand, are made up of thousands of cores. While they can’t perform the type of complex tasks that a CPU can, they are highly optimized for simpler tasks like floating point and integer computation. This is particularly useful for graphics rendering and generative AI training which depends on loads of matrix arithmetic that can be processed non-sequentially.

In the past few years, there has been a significant increase in GPU intensive products. The release of ChatGPT in 2022 put pressure on companies across many sectors to develop AI tools in order to stay competitive. Advances in high-quality graphics rendering in the entertainment industry and AR/VR have set new standards for visual quality among consumers. Additionally, 3D modeling has allowed for more efficient workflow in the architecture, sciences, automobile and medical industry.

These innovations have led to a sharp increase in demand for GPUs. The GPU market was valued at USD 44.7 Billion in 2022 and is projected to reach USD 450.9 Billion by 2030.

So, this must mean every company is buying up GPUs, right? Not quite. The demand is there, but GPUs don’t grow on trees. Supply for the latest GPUs is limited, and building AI models from scratch requires thousands of high-end GPUs. Furthermore, the best GPUs are quite expensive. This isn’t a huge problem if you are a mega-rich tech company, but it is quite a problem for everyone else.

For context, it took two thousand and forty eight (2048) A100 80GB GPUs to train Meta’s large language model (LLaMa). At $15,000 per GPU, this comes out to about $30mil in hardware expenses. It’s estimated that ChatGPT, the mother of all AI, requires 30,000 A100 GPUs to handle daily inferences (user inputs) alone.

If GPUs are so expensive and inaccessible, what are the little guys to do?

Solution: Rent from the big boys.

In data centers across the world, cloud providers like Microsoft, Amazon and Google host insane amounts of GPUs and CPUs, which in turn are rented out to companies around the world.

Cloud computing is a huge industry. According to Statista, in 2024, the global public cloud services market is expected to grow by approximately 20.4 percent, which amounts to about 679 billion U.S. dollars.

The benefits of going to AWS/Azure/GCP for cloud computing is they provide a full stack solution with compute, storage, data lakes, dev tools and more. This is appealing, and works for most companies. However, they’re gonna rake you over the coals on pricing, and take you off their platform if they don’t like you.

Thanks to distributed networks, there are alternative options. Companies like Akash and Render have created networks of independent suppliers, ranging from independent data centers with underutilized compute to 3D artists who are in between projects. The concept is similar, but instead of getting your compute resources from a warehouse owned by Microsoft, you get it from nodes in the network.

Using decentralized compute platforms like Render or Akash, you can get quick access to industry standard GPUs for <50% the cost. Here’s a comparison of A100 80GB rentals:

Pricing Breakdown:

Amazon (AWS): $4-5/hr

Microsoft (Azure): $3.50-4/hr

Google (GCP): $3.50/hr

Akash: ~$0.79/hr

Render operates on a “per job” model where users do not rent specific GPUs, but rather pay per job. A better pricing comparison for Render is comparing against traditional “render farms”. Turns out Render is >50% cheaper.

Aside from pricing there are additional benefits one gets when choosing the decentralized route, but we’ll get into those later.

While there’s been a recent influx of decentralized compute protocols (most of them riding the narrative), the two biggest players both by market cap and by utilization are Render and Akash.

One would think that the two largest players in this niche must be direct competitors. All indications on social media have led me to deduce that this is the commonly held belief in the crypto community. Disproving this is one of the primary drivers behind writing this article.

I’d like to first talk about positioning because I believe this is the most fundamental difference. Covering positioning first should help provide context to their value propositions and growth metrics.

While we go over the differences, keep in mind these “first principles” similarities between the two protocols.

Similarities:

Both function as a distributed network comprised of independent nodes

Both allow users to rent computational resources from said nodes

Both accept cryptocurrency as a form of payment

Both are listed within the AI and DePIN categories on CoinGecko

Render vs. Akash

Positioning

The most fundamental difference between Render and Akash lies in their sector positioning. Although both protocols operate distributed networks for renting computing resources, their target users have minimal, if any, overlap.

Render’s offering specifically targets digital creators. Scroll down a bit on their landing page and you will see in large bold type:

“The Render Network® Provides Near Unlimited Decentralized GPU Computing Power For Next Generation 3D Content Creation.”

Thanks to industry connections established through their parent company OTOY, they are already widely recognized among creators. They have supplied computing resources to a diverse array of creators, ranging from major film studios such as Paramount and HBO to independent 3D artists like Beeple and David Brodeur. Their primary product offering lies solely within this niche.

Akash's offering is developer-based. Developers lease computational resources from their cloud marketplace and can deploy their applications on Akash's container platform. The majority share of Akash's rental volume consists of CPU resources. While Akash is currently expanding its GPU offerings to cater to AI developers, this initiative is still in its early stages. Render, on the other hand, does not offer CPU resources at all.

Another common misconception in the competitive landscape arises from the AI narrative associated with each protocol. This misunderstanding regarding their AI offerings is primarily one of semantics.

Due to AI’s consumer impact, when people hear "AI," they often associate it with large language models like ChatGPT or text-to-image models such as DALL-E. However, AI is an incredibly powerful tool for 3D modeling across a variety of creator industries, including art, entertainment, gaming and architecture.

Where Akash’s AI-based GPU offering is aimed towards developers, Render’s direct AI offering is tailored to creators.

Render is tangentially competitive in developer-based GPU, but this extends only so far as to provide extra nodes to 3rd party AI/ML compute protocols like io.net.

Value Propositions

Now that each protocol’s sector positioning is clear, their respective value propositions can be more easily understood.

Render’s Value Propositions

Aside from better pricing, Render’s value prop can be summarized in three main points:

Significantly increased render speed

Seamless integration with industry standard software

On-chain provenance for digital rights and royalty distribution

Render Speed:

Spreading the rendering work across multiple nodes in the network allows for frames to be rendered in parallel, significantly reducing the time required to complete a rendering job. It’s hard to calculate exactly how much time is saved offloading to Render Network since their model operates on a “pay-per-job” basis and depends on a variety of technical factors like hardware specs and compute required. However, for some context, let’s look at a testimony by prominent 3D artist Brilly:

It cannot be overstated how beneficial this is for creators operating on a limited budget and facing hard deadlines. By reducing rendering time, creators can undertake more projects, increase their income, and advance their career at a faster pace.

Software Integrations:

Since its inception in 2008, OTOY, Render’s parent company, has been a leading force in cloud graphics. OTOY’s OctaneRender plugin is integrated into industry-standard content creation software, like Cinema 4D, allowing for a seamless one-click export of ORBX files to the Render Network.

This integration provides a low-friction experience for users, many of whom are already familiar with OTOY’s products. These fundamental web2 integrations are very rare in crypto, giving Render a strong moat when it comes to market positioning.

Digital Right & Royalty Distribution

One of the most frequently overlooked benefits to using the Render Network is on-chain provenance.

Each time a user uploads a scene and a node operator processes a job on the Render network, all assets and settings in the ORBX render graph are hashed. This ownership data can be used to set up IP rights and restrictions, opening the door to future innovations such as automated royalty processing.

Akash’s Value Propositions

Now, let’s take a look at Akash’s non-cost related value propositions:

Censorship resistant hosting

Flexibility and customization of resources

Payment optimization & crypto-native payments

Censorship Resistance

In 2021, the right-wing social media platform Parler was booted from AWS for allegedly violating their terms of service. Regardless of where you fall on the political spectrum, it’s naive to believe that the centralization of cloud providers doesn’t pose potential threats to freedom of speech.

Akash’s compute leasing is fully permissionless, meaning unless every node in the network collectively decides not to host your content, you won’t face any risk of being deplatformed.

Flexible & Customizable Resource Allocation

One of the issues developers face when deploying their application to the cloud is “vendor lock-in”.

Vendor lock-in is when a user is essentially forced to continue using a product or service regardless of quality, because switching away from that product or service is not practical. In cloud computing, the consequences of vendor lock-in are often that the provider raises prices, or changes their offering, knowing that migration from their platform is not practical and requires moving and reformatting data to a new environment.

Akash’s deployment platform is optimized for hosting and managing containers, which are standardized units of software that encapsulate code and all its dependencies. Because containers are self-contained and isolated from the underlying infrastructure, they can run consistently across different environments.

This means that developers can create their applications within containers and deploy them on Akash's platform without worrying about future compatibility issues.

Payment Optimization

Compared to traditional providers, Akash offers a unique pricing model. Instead of providers setting a price for resources, developers make offers based on their budget and needs.

This system, known as a “reverse auction”, creates dynamic supply and demand pricing, empowering developers to tailor their offers within their budget constraints.

An important crypto-native benefit of Akash is that all payments are made in either their native token AKT or USDC. This is particularly beneficial for developers who may not have access to traditional payment rails.

In a recent interview, Greg Osuri highlighted a case where a developer from Africa, who lacked access to a bank, was able to deploy their website on Akash with AKT sent from a friend.

Satoshi’s vision.

Growth Metrics

Note: Crypto valuations are highly speculative and fundamentals are often a mid-curve meme. Take the following with a grain of salt.

As previously discussed, from a positioning and value proposition standpoint, Render and Akash are apples to oranges.

However, markets are not rational, and many market participants will likely continue to make an apples to apples comparison. Let’s temporarily take the position that they are direct competitors and run the numbers.

Gathering data for Akash was easy, as they provide a stellar dashboard for tracking metrics. However, Render’s metrics are a bit more opaque.

I was able to pull 2023 metrics from Render’s 2023 Render Network Metrics article, as well as quarterly updates published on their Medium. Due to the unavailability of more recent data, the following analysis is based primarily on 2023 metrics.

Let’s start with their current market caps - April 5th, 2024; then we’ll dive into the fun-damentals:

Render:

Market Cap: 3.5bil

FDV: 4.9bil

Market Cap / FDV: 0.72

Akash:

Market Cap: 0.95bil

FDV: 0.96bil

Market Cap / FDV: 0.99

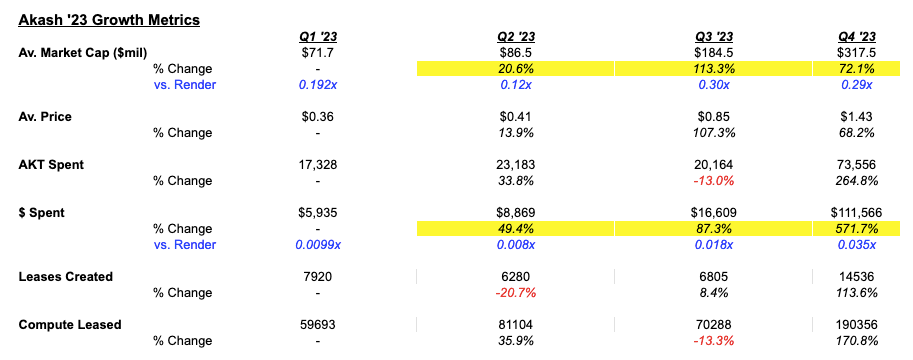

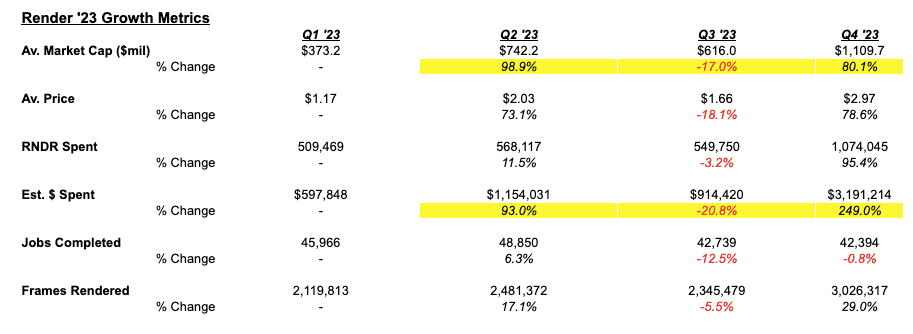

From a relative market cap perspective, not much has changed since late last year. Akash’s market cap currently sits at 0.27x that of Render’s, remaining relatively in line with the Q3’23 & Q4’23 ratios (0.30x & 0.29x).

Narrative Confluence:

Both networks saw a ~4x pump from their Q4’23 market caps, primarily driven by the “rising tides lifts all boats” nature of sector-specific narratives in crypto - in this case AI and DePIN.

If AI and DePIN narratives remain strong throughout the rest of the bull run, it wouldn’t be surprising to see continued strength for both AKT and RNDR.

Additionally, RNDR benefits from the current “Solana narrative”, further strengthening its “narrative confluence”. Maybe we’ll finally see a Cosmos narrative that pumps Akash later on? Gotta take that one up with their marketing team.

Network Growth:

In regards to network growth, the two metrics I want to focus on are:

$ transacted on the network (GMV)

Number of jobs / leases created (User Demand)

Available compute is another important metric to consider. However, as of yet, neither Render nor Akash have faced supply constraints. At present, Akash’s usage is only ~30% its full network capacity. Render provides compute for multiple 3rd party clients and has a waitlist for new direct providers.

Note: Render Network's precise quarterly spend in dollars is not explicitly provided. I estimated it by multiplying the average token price each quarter by the quantity of Render tokens spent, as reported by Render Foundation. I validated this estimation by applying the same method to Akash. The resulting estimations closely matched the USD spend reported on Akash's dashboard. In the model below, Akash's USD spend is from their dashboard metrics, not the estimation method.

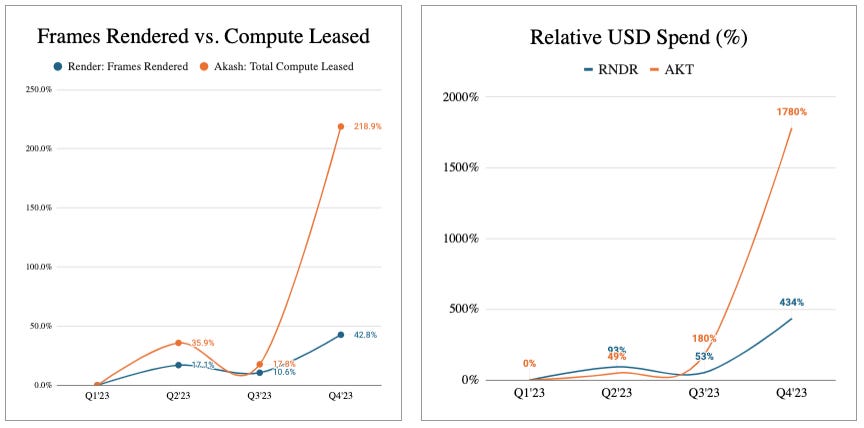

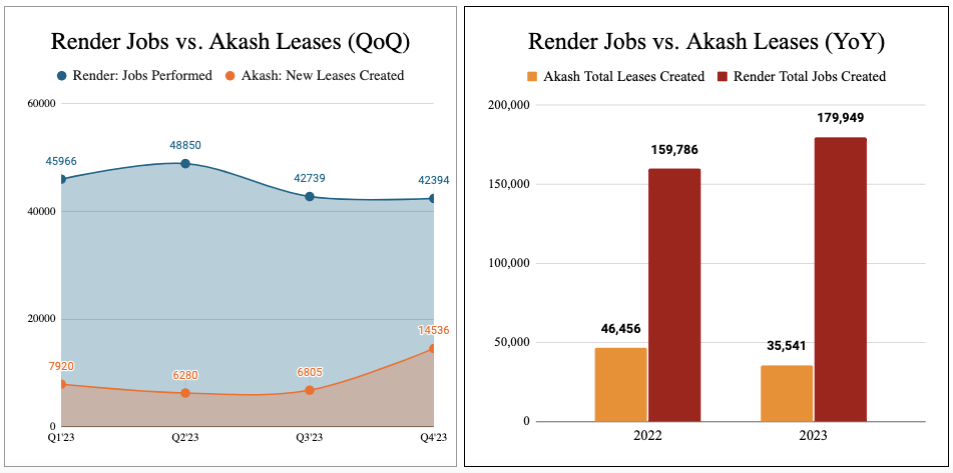

To get a rough picture of user demand, I’m comparing render jobs created on Render vs. leases created on Akash. It’s not perfect, but turning an orange into apple juice is the job at hand.

This metric is further broken down into total frames rendered on Render and total compute leased on Akash to understand the resources consumed from jobs and leases.

GMV Insights

Render has a strong lead in absolute GMV

Through 2023 Akash captured a maximum of 3.5% Render’s GMV

Akash is outpacing Render in relative GMV growth

From Q1-Q4 Akash’s annualized GMV increased by 17.7x vs. a 4.3x increase in Render’s annualized GMV

Both Akash & Render saw the strongest QoQ growth in Q4, with Akash growing GMV by 5.7x and Render by 2.5x

Akash’s significant Q4 GMV growth can be partially attributed to its introduction of GPUs to the network, which require higher spend

Despite Akash’s av. market cap growing from 0.19x to 0.29x that of Render’s, Akash’s premium to Render declined, from 19x in Q1 to 8x in Q4

User Demand Insights:

From 2022-2023, leases created on Akash declined by 23% while Render jobs increased by 11%

Despite Akash’s 2022-2023 YoY decrease in leases, in 2023 it overall exhibited stronger QoQ lease growth compared to Render’s QoQ job growth

Throughout 2023, jobs on Render and leases on Akash showed a near symmetrical divergence

After an initial 6% increase from Q1-Q2, Render jobs dropped by 12% in Q3 and remained relatively stagnant the rest of the year

Akash leases declined by 20% from Q1-Q2, but surged by over 130% in the second half of the year

Frames rendered on Render saw a 42% increase vs. a 219% increase in compute leased on Akash

The divergence in frames rendered and jobs completed on Render in Q3-Q4 is primarily due to large scale one-off projects such as the first rendering jobs for the Las Vegas Sphere and the Apple Vision Pro.

Note: RNDR in Blue, AKT in Orange.

If one chooses to make an apples to apples comparison, it’s evident Render has a strong lead in total GMV, but Akash is slowly catching up.

Both are miles away from the big three centralized players. Per Canalys data, worldwide cloud infrastructure services quarterly spending was $73.5bn in Q3’23, with Microsoft capturing 25% ($18.4bn) of that spend.

In Q3’23 Render’s total spend was $914,420 and Akash’s total spend was $16,609. For Render, that’s about 0.0004% of Microsoft’s spend. For Akash, it’s 0.0000009%.

But, for the sake of our industry, let’s all agree to never speak of this last point.

Concluding Thoughts

I hope by now I’ve done a halfway decent job at presenting the perspective that comparing Render to Akash is more of an apples to oranges comparison than an apples to apples comparison.

Of course, crypto is incredibly speculative and basing one’s investment decisions on “fundamental analysis” can, non-ironically, be detrimental to making money in this space.

So, do with this information what you will!

Ride the wave of euphoria which I believe is still yet to come, invest more than you can afford to lose, and if this information was interesting or helpful in any way, let me know what you’d like to see next!

This was an extremely thorough analysis and all around great read. I’m looking forward to reading more content 🔥

One of the best non nonsense break downs of Akash and Render value propositions. It's refreshing to read a comparison like this from a person who actually knows what he talks about instead of "fan mooooonbois". Great stuff!